The Carpetbagger’s Guide to Home Ownership

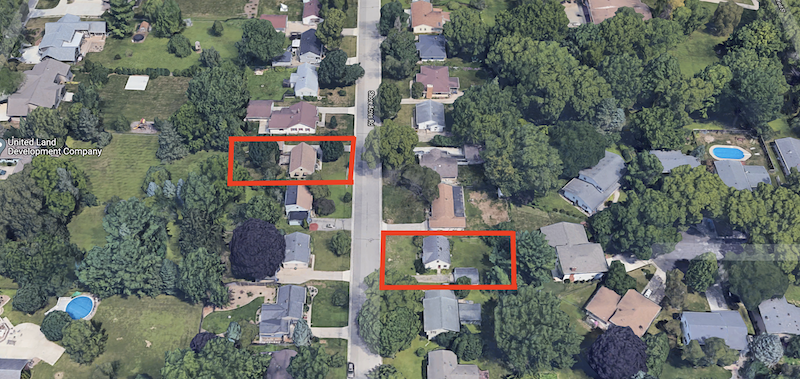

In March I bought a modest house in Madison, Wisconsin as a rental property. I worked with good local professionals to bring that house up to a better standard and in July I found excellent high quality tenants. We have cordial relations and I’m confident they feel they’re getting excellent value for their money and are happy in their new home. That property is now contributing to my long term diversified retirement plan. Along the way I took an aging home that needed some love and gave it new life.

Then in October, much to my surprise, I bought a very similar house right across the street from the first one. I’m now employing the same group of local trades to renovate it as well. If all goes to plan it should be rented by spring to equally qualified and respectable tenants.

In a perfect world I’d much prefer to use my financial resources to build genuinely affordable new housing which society desperately needs. But this isn’t a perfect world. It’s decidedly imperfect. I learned that the hard way. So I’m essentially reaching back into the past and shining up the leftovers from a previous era.

My real estate agent Ben was instrumental in these transactions. Not only did he identify the right properties for me, but he helped assemble a team of trusted trades to upgrade the mechanical systems, paint, install solid wood floors, new appliances, countertops, look after the landscape, and so on. I honestly couldn’t have done any of this without his guidance or the great people he introduced me to. The first project was such a smooth experience that it gave me the confidence to move forward with the second sooner than I might have planned.

Ben recently invited me to be on his podcast on the topic of real estate investing. I hesitated. I didn’t want to be perceived as the token out-of-state carpetbagger driving up housing costs for locals and pushing up rents. The problem, of course, is I might be exactly that… So I asked if we could take a different approach.

Instead of me talking about my real estate activities as a comfortably middle aged guy with some extra cash to deploy, what if we had a conversation about how I first bought property when I was much younger and infinitely poorer? If I somehow managed to buy property in a crazy expensive place like San Francisco on a super tight budget that might help people in Madison explore their own options in a more moderate economic environment.

There are alternative routes to acquiring real estate for those feeling the squeeze. Being angry at investors or landlords doesn’t get people into the housing they need. Understanding the institutional structures of real estate and exploring creative work-arounds just might. I’ve written about my adventures in property before, but the subject matter is worth repeating. These options may not appeal to everyone, but they worked for me.

I’ll start off by saying I’m a housekeeper. I clean other people’s homes for a living. Are we clear on this? I’m a maid. I grew up in an unstable household that limped from crisis to crisis. I dropped out of high school, left home, and moved to the other side of the country. Leaving allowed me to find more fertile soil to plant myself, and my absence meant one less problem for the family to deal with.

When I first arrived in San Francisco I lived in a variety of “alternative” accommodations including this little 9’ x 18’ (15 m²) garden shed behind an old Victorian in a questionable neighborhood. There was a toilet and a shower stall in a little closet in one corner, and a minimal kitchenette in the other. There was just enough room for a bed and a cafe size table. It was affordable on my housekeeper’s income and I loved having a diminutive place of my own.

It was also sub rosa and illegal like most truly affordable housing in San Francisco. Nothing about this place met minimum code requirements or zoning parameters, yet it was perfectly safe and healthy. I sanded and varnished the old wood floors, painted the walls, installed a few cabinets, and generally personalized the space while I lived there. It was a fantastic spot that I’m still a bit nostalgic about decades later. The shed was never about the things I didn’t have. It was about the freedom it gave me.

Living frugally afforded me the wiggle room I needed to save money each month. For example, I didn’t own a car back then. People rarely consider how much money a vehicle chews up and how those funds could be redirected toward saving for a home. Choosing to live in a place where it’s physically possible to get around on foot or a bicycle can make real estate more attainable more quickly. Even switching from a two car household to a one car household makes a huge different when funds are tight. Not everyone can or will embrace this concept, but it worked for me.

As a young self employed housekeeper looking to buy property in San Francisco I quickly realized it just wasn’t going to happen. The numbers involved were simply too big. I didn’t want to leave the city and the opportunities and culture it provided. But I didn’t want to wake up thirty years down the road and find myself aging and broke. Poverty is no fun. So I made a plan to buy property far enough away that it was affordable and use that house as my retirement destination. In the meantime it could be used as my personal vacation home or income producing rental property while I continued to live modestly in rented space in the city.

Given my economic and social status no bank would give me a mortgage or construction loan. So I paid cash for a vacant plot of land out in the countryside and gradually built a one room 480 square foot (44 m²) cabin on a cash basis over a number of years. The cabin was my “car” as far as my budget was concerned. Car loan payments, insurance, tires, repairs, gas… All that vehicle money was redirected toward my goal of home ownership.

The house was bare bones and fitted with makeshift second hand furniture, but it did everything I needed at a price I could manage without debt. Compared to the tiny shed I was living in back in the city It seemed palatial. This was by no means a simple process. I learned a lot about building codes and the difficulties of do-it-yourself construction along with the joy and pain of managing tenants once the place was completed. But it got me on the first rung of the property ladder. Owning a mortgage free home with a bit of rental income gave me the security I needed for my future. This may not be everyone’s cup of tea, but it worked for me.

While I was living in the garden shed in the city and managing the country cabin I began to hatch a plan to buy a place in San Francisco by any means possible. Again, it was about long term security rather than any kind of investment strategy. As a housekeeper I sometimes work for people who own rental properties and I became aware of a small apartment building that one of my employers was thinking of selling.

Housekeepers tend to get passed around by word of mouth so I happened to clean for a few of his tenants at that particular property. I also knew that each of those tenants was planning on moving out for various reasons - one for a job abroad, one to get married and buy a house, etc.

I organized a group of friends who were equally young and also wanted to buy real estate in the competitive San Francisco market. I proposed we pool our resources and buy the multi-unit property collectively. There’s an economy of scale associated with buying a single structure compared to five separate small homes or five scattered condos. The cost per apartment is significantly lower when bought in bulk. Plus, a collective purchase with a group of friends meant dividing the down payment and monthly expenses into smaller more manageable portions.

I was already a known quantity to the landlord so he felt comfortable renting to me in a way a stranger might not. As each additional apartment became vacant I arranged for my friends to occupy the empty units one by one. Once we were all settled in we got our ducks in a row and approached the owner about buying the place - something he was already inclined to do. There would be no drama with rent controlled tenants or evictions, and the sale would be smooth since everyone was on the same page and already physically in place.

But once again, no bank would give us a mortgage. A property that has four or fewer apartments is treated the same as a single family home for lending purposes. But five or more units requires a commercial loan. So we created a pro forma and told the bank we were investors looking to be slumlords and this building would cash flow. They loved that idea! Because… that’s how the world works.

The landlord did the math and agreed to sell to us at below the full market value. He would be saving so much money by avoiding the associated legal challenges from disgruntled tenants that he would net the same profit even at a slightly lower price. We secured the commercial loan and quietly went about renting the apartments to ourselves.

Each apartment’s share of that single monthly loan payment was $900. There were two of us living in our apartment so my boyfriend (now husband) and I were paying $450 each. That was less than the rent on my old garden shed. It’s been quite a while and we’re all still here. Chipping in to buy this place was by far the best financial decision any of us have ever made. I understand this kind of arrangement is absolutely not for everyone, but it worked beautifully for us.

Some time passed and I set my sights on an additional property. We have friends in Sonoma County north of San Francisco and it’s a really beautiful area. But, of course, lots of people want to live there so it’s seriously expensive. We saved, we poked around at properties in a casual Looky Lou sort of way. It was more daydreaming than anything. Then the 2008 crash occurred, prices dropped dramatically, and suddenly we were in a position where we actually could afford at least some scratch and dent real estate in Sonoma.

We had cash saved up at a time when most other people were overly leveraged and struggling to stave off foreclosure. We bought the smallest most run down house on the market at a bargain basement price and gradually began fixing it up. Once it was habitable we rented the house to good people. We had a small mortgage for the first few years, but paid it off quickly.

Now that we’re in our fifties we have a really low burn rate at our primary residence in the city. We have steady revenue coming in from our past investment properties. And we’ve got very little debt with high savings. I’m still a housekeeper because I need something to do with my time, but my husband’s career has matured to the point where there’s extra cash to mobilize for things like a couple of fixer uppers in Madison.

Why Madison, you ask? It’s got the right combination of relatively affordable real estate and relatively high rents with a generous supply of solvent high quality renters looking for respectable accommodations. Plus we have family in the region. Wisconsin is also outside of California’s earthquake and forest fire zones. Wisconsin has other risks like tornadoes, but they’re different so we feel we’re diversified.

The stock market can go up or down, real estate values can spike or crash, cryptocurrencies can take over the world or be revealed as just another Ponzi scheme, gold might be a “barbarous relic” or a safe haven… I have no idea. I really don’t. But one way or another these properties will help keep us warm and dry.

So here’s a quick review for the folks out there who are pissed off about the high cost of housing and feel locked out.

1) Consider living below your means and doing without certain things in order to make saving for a house the bigger priority.

2) If you can’t buy in the expensive location you really want, buy elsewhere. Then find a way for that property to generate income while you continue to be a renter yourself in the more expensive spot.

3) Work cooperatively with like minded people to buy a share of a building collectively in a mutually beneficial arrangement.

4) Save and prepare for the next market correction. There’s ALWAYS another crash on the horizon - and that’s a good thing. You can’t time the market on the way up, but you know for certain when the crisis hits. Then scoop up a bargain.

5) You don’t need as much house as you’ve been lead to believe. Instead of trading up for a larger fancier house with more debt as you age, consider living simply and buying additional homes for diversified income.